As the country’s housing stock ages and new homes remain out of reach for many consumers, remodeling is gaining a larger proportion of the residential construction sector, both in terms of enterprises and employment.

With the majority of American households unable to finance new construction, rehabilitation has become a more feasible and cost-effective option for improving housing conditions, fueling consumer demand.

On the supply side, many home builders work on renovation projects to expand their business.

According to NAHB’s examination of Quarterly Census of Employment and Wages (QCEW) data over the last quarter century, the rise of remodelers indicates a long-term structural shift rather than a brief post-pandemic boom.

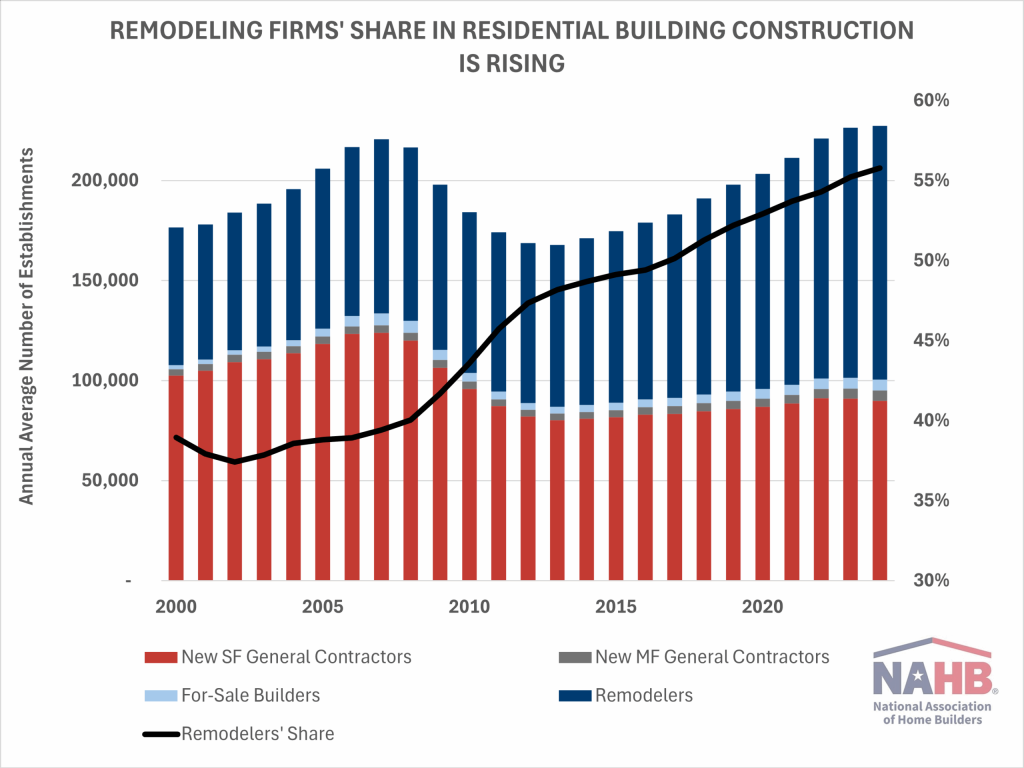

Remodeling Firms’ Share of Residential Construction is Rising

Over the last 25 years, the number of renovation businesses has nearly doubled—from fewer than 69,000 in 2000 to more than 128,000 in the first quarter of 2025.

Remodelers currently account for more than half (56%) of all residential building construction (RBC) companies.

Remodelers’ share, in contrast, regularly hovered at 38-39% throughout the mid-2000s housing bubble, when the market was dominated by home builders, including new single-family and multifamily general contractors, as well as speculative (spec) home builders.

Although the renovation industry was not immune to the 2008 housing meltdown, its losses were small in comparison to the contraction of home construction.

Between 2007 and 2012, the number of renovation companies decreased by 8%, while nearly one-third of home builders went out of business.

As a result, the remodeler’s proportion of the RBC industry increased dramatically following the recession, reaching 46% in 2011, and has risen continuously since then.

Both remodelers and home builders witnessed significant expansion during the post-pandemic housing boom, which was fueled by cheap mortgage rates, the development of remote work, and a renewed need for larger living areas.

Remodelers, on the other hand, grew at a higher rate, with their share of RBC enterprises reaching 54% in 2022.

Remodelers, who are less vulnerable to mortgage rate swings than home builders, have continued to thrive despite a series of aggressive Federal Reserve rate hikes that have dramatically boosted the cost of home purchases and delayed new building. By 2024, renovation businesses will account for 56% of all RBC locations.

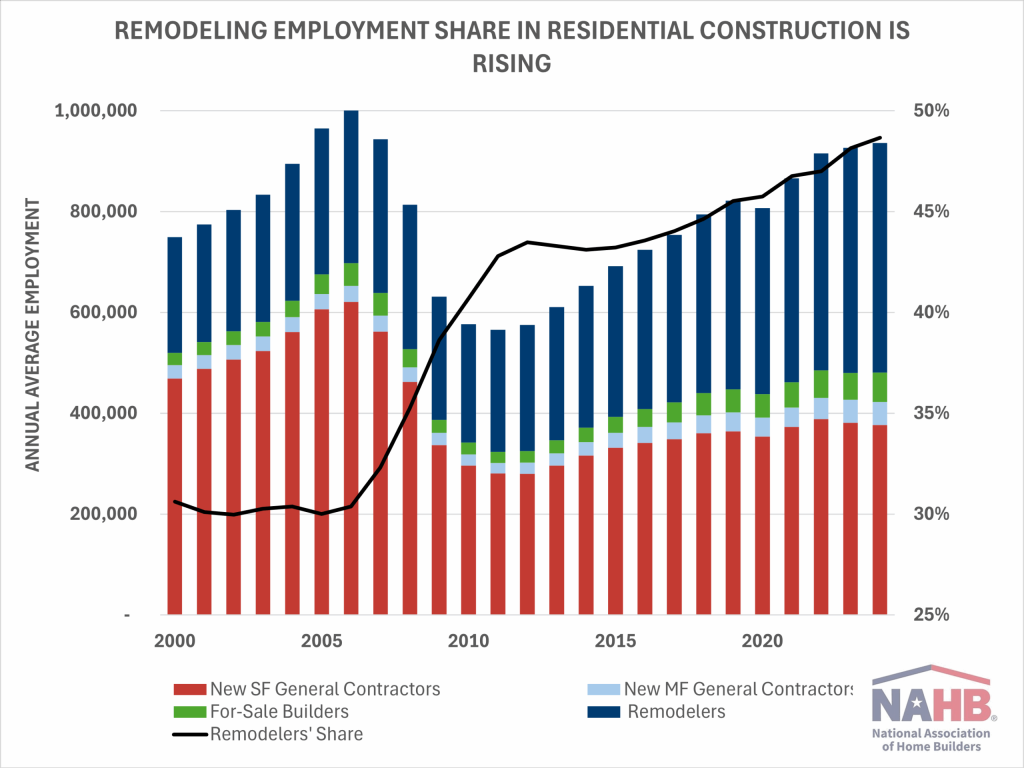

RBC’s remodeling employment share is increasing

The construction industry as a whole, which includes residential and non-residential building construction, heavy/civil engineering construction, land subdivision, and specialty trade contractors, is dominated by the latter. However, government employment surveys cannot determine how much of a subcontractor’s business is committed to renovation. As a result, RBC is the subsector that best captures renovation trends.

The research of employment trends in residential building construction finds a similar pattern, with remodelers creating a growing number and percentage of jobs, primarily at the expense of single-family general contractors.

In 2024, the renovation sector employed about half (49%) of RBC employees. During the mid-2000s housing boom, just 30% of payroll employees worked for remodelers, while single-family general contractors employed 63% of RBC’s staff.

The change is considerably more significant among the RBC industry’s production (nonsupervisory) personnel.

According to the NAHB’s examination of historical data from the Bureau of Labor Statistics’ Current Employment Statistics (CES) survey, more than half (51.2%) of these skilled craftsmen now work for renovation firms, up from about 30% in the early 2000s.

Multifamily general contractors, who subcontract the majority of their construction work, account for a lower share of home building jobs, although they have gained ground.

Strong multifamily activity in 2022-2023 increased their share of RBC employment to 5% by 2024. An additional 6% goes to builders who develop for sale.

The median remodeling firm remains modest, with 3 to 4 people per location, close to levels seen during the mid-2000s housing boom. This stability indicates that the total increase in remodeling employment is mostly due to the formation of new firms or the reclassification of home builders as remodelers.

As market conditions change, some home builders, particularly smaller single-family general contractors, are likely to shift their focus to rehabilitation projects in order to stay in business and develop.

The remodeling sector’s lower entrance barriers, lesser initial investments compared to new building, and fewer regulatory impediments facilitate the shift.

As more businesses see remodeling as their major activity and revenue source, they will be classed as remodeling establishments in official data reporting.

The North American Industry Classification System (NAICS) guides data collecting in the United States. Under NAICS, a corporation self-classifies and selects the industry code that best describes its principal business activity.

In some surveys, such as the Economic Census, the Census Bureau prioritizes revenue sources as a main criterion for identifying firms.

The continually increasing number of remodelers and the employment they produce demonstrate that remodeling has become a dependable engine fueling growth in the residential building sector.

[Read more about this topic on Eyeonhousing.org]