According to NAHB’s quarterly Land Acquisition, Development, and Construction (AD&C) Financing Survey, the cost of credit for residential construction and development fell in the fourth quarter of 2025.

The average contract rate fell on all four categories of loans tracked in the survey, from 7.95% in the third quarter to 7.61% on loans for land acquisition, from 7.68% to 7.44% on loans for land development, from 7.89% to 7.47% on loans for speculative single-family construction, and from 7.90% to 7.16% on loans for pre-sold single-family construction.

Meanwhile, the average initial points paid by builders and developers decreased on three of the four types of AD&C loans: loans for land development fell from 0.83% to 0.44%, loans for speculative single-family construction fell from 0.75% to 0.34%, and loans for pre-sold single-family construction fell from 0.67% to 0.37%.

The only exception was loans for land acquisition, for which the average beginning points increased slightly—from 0.66% to 0.70%.

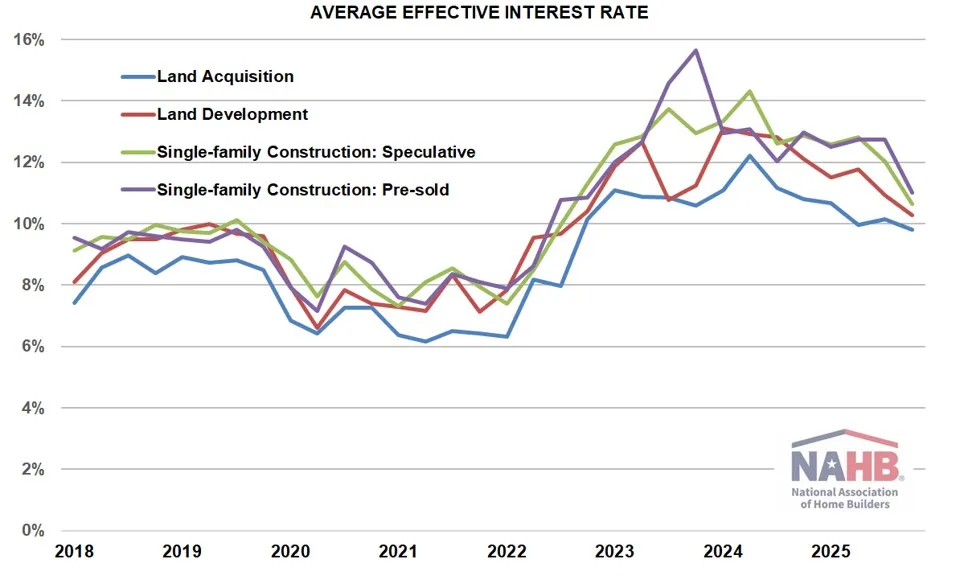

The average effective interest rate, which accounts for both the contract rate and initial points, decreased overall from 10.15% to 9.81% on loans for land acquisition, from 10.92% to 10.28% on loans for land development, from 12.04% to 10.64% on loans for speculative single-family construction, and from 12.74% to 11.01% on loans for pre-sold single-family construction.

This was because the slight increase in points on land acquisition loans was insufficient to counteract the decline in the contract interest rate.

In all four cases, the average effective rate was the lowest since the period of usually rising interest rates in 2022.

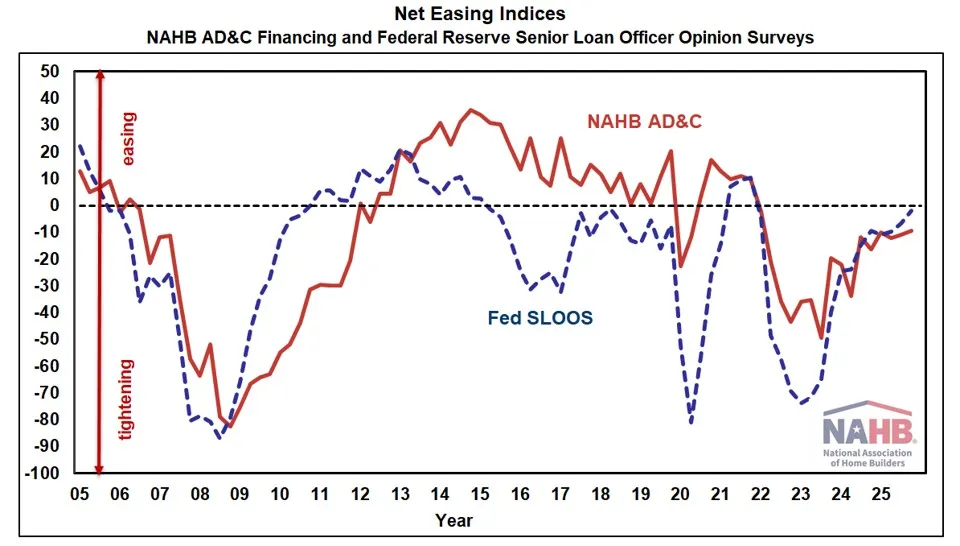

Despite the rate decline, builders and developers continued to report tightening lending circumstances in the fourth quarter of 2025.

The net easing index calculated from NAHB’s AD&C survey was -9.3 (a negative figure indicating that credit has tightened since the previous quarter).

This is consistent with the results of the Federal Reserve’s study of senior loan officers. In the fourth quarter, the Fed survey’s net easing index had a -1.8 level.

For the 16th straight quarter, both the NAHB and Fed surveys have shown tightening credit conditions.

However, in both situations, the net easing index in Q4 2025 was closer to the zero break-even point (between tightening and relaxing) than it had been since the first quarter of 2022.

Furthermore, according to the NAHB AD&C survey, 35% of respondents who built single-family houses in the fourth quarter of 2025 financed some of the building using a construction-to-permanent (one-time-close) loan issued to the ultimate home buyer.

On average, 59% of the residences constructed by these respondents were financed in this manner.

The NAHB’s AD&C Financing Survey web page provides more information on lending conditions for residential builders and developers.

[Read more about this topic on Eyeonhousing.org]