According to NAHB’s analysis of the most recent 2024 data from the American Community Survey (ACS), the construction labor force is currently transitioning from construction trades to management, business, and technical positions, a trend that has been in progress for some time.

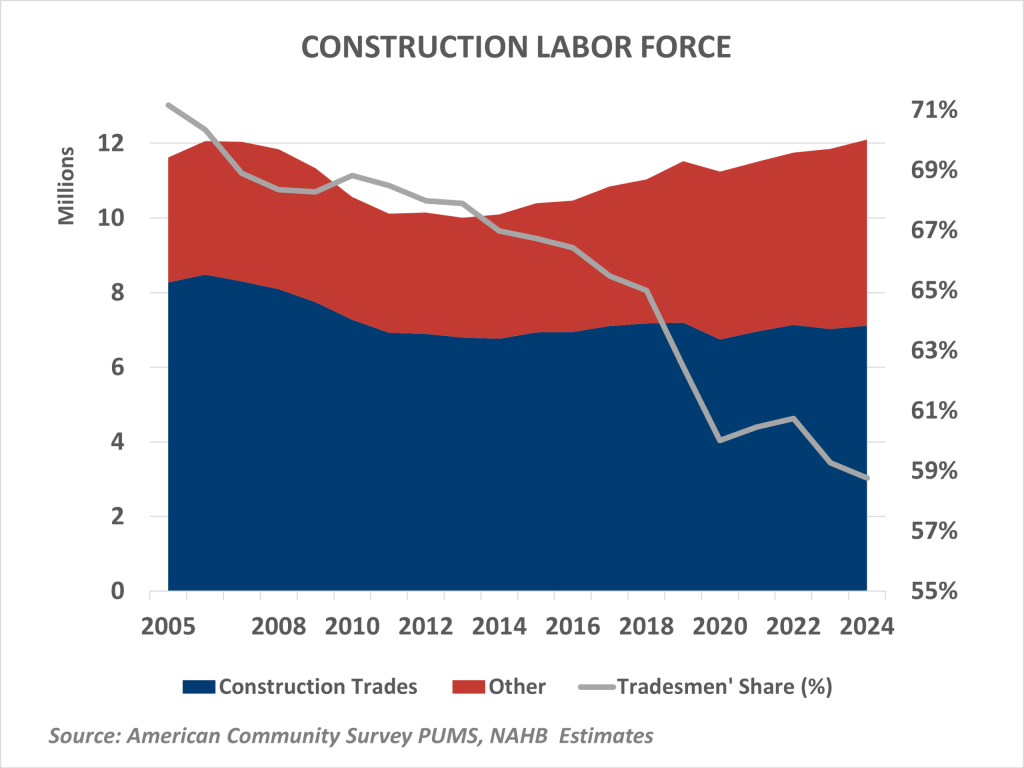

Despite the fact that the total industry employment now marginally exceeds the levels achieved during the 2005–2006 housing boom, the composition of that workforce has undergone a significant change. The proportion of construction trades laborers has decreased from 71% in 2005 to less than 59% in 2024.

Simultaneously, the proportion of occupations in the fields of computer science, engineering, and science has increased by over twofold, while management and business positions have expanded by 73%.

In the context of persistently modest productivity growth in construction, these shifts are particularly striking.

In theory, productivity enhancements should be facilitated by an increased number of engineering and technology professionals, who will contribute to enhanced project design, coordination, and innovation.

Nevertheless, the expansion of management and business roles may also be indicative of the escalating complexity of regulatory requirements, permitting requirements, and compliance costs.

These factors can result in a delay in project completion and an increase in administrative costs without a direct increase in output.

The productivity benefits may also be counterbalanced by the decreasing proportion of skilled trades workers, who are the group most directly responsible for on-site production.

Collectively, these compositional modifications confound the relationship between productivity and workforce structure.

The construction labor force has surpassed 12.1 million workers as of 2024, which is a modest increase from its peak in the mid-2000s.

7.1 million workers, or 58.8% of the total, are employed in the construction professions, which include carpenters, electricians, painters, plumbers, laborers, and first-line supervisors.

In contrast, the peak of 2006 was characterized by the presence of 8.5 million trade laborers.

The persistent labor shortages documented in the NAHB/Wells Fargo Housing Market Index (HMI) Survey are partially accounted for by the loss of over one million tradesmen.

An increasing number of white-collar workers have been assimilated by the industry during the same period.

The proportion of workers in management echelons increased from 10% to 17%, as they expanded from 1.2 million to 2 million.

The growth rates of financial and business occupations were comparable.

In the interim, the proportion of individuals employed in engineering, architecture, and science-related occupations has more than doubled, reaching nearly 2.8% of the workforce, a significant increase from the 1.3% reported in 2005.

Despite these advancements, the construction industry continues to have a lower prevalence of white-collar positions than the broader U.S. economy. Nevertheless, their expansion has exceeded the tempo of national developments.

For instance, the proportion of occupations in the fields of computer science, engineering, and mathematics increased by over twofold in the construction sector, while the overall U.S. workforce experienced a 48% increase.

In the same vein, the proportion of legal and design occupations in the construction sector has doubled, despite the fact that their economy-wide presence has only increased by 20% since 2006.

These trends are presumably the result of a combination of structural factors. The demand for technical expertise has been bolstered by advancements in construction technologies, such as prefabrication, project management software, and digital design.

Simultaneously, the necessity for administrative, compliance, and managerial functions has been exacerbated by an increasingly stringent regulatory and building code environment.

The declining self-employment rates in construction are also consistent with the changing workforce composition, which implies a transition to larger firms.

These companies are typically better equipped to invest in new technologies, manage regulatory complexity, and sustain increasing overhead costs.

The ACS Public Use Microdata Sample (PUMS) is the source of the labor force statistics presented here, which offers comprehensive coverage of both payroll employees and the self-employed. These estimates encompass both employed individuals and those who are actively pursuing employment, in accordance with conventional labor force definitions.

[Read more about this topic on Eyeonhousing.org]