Despite historically low self-employment rates and the growing market share of the top 10 builders, independent entrepreneurs continue to dominate the residential construction industry, accounting for approximately 80% of home builders and specialty trade contractor firms.

Even among firms with paid staff, small enterprises continue to dominate the market, with 63% of homebuilders and two out of every three specialist trade contractors generating less than a million dollars in total business revenue.

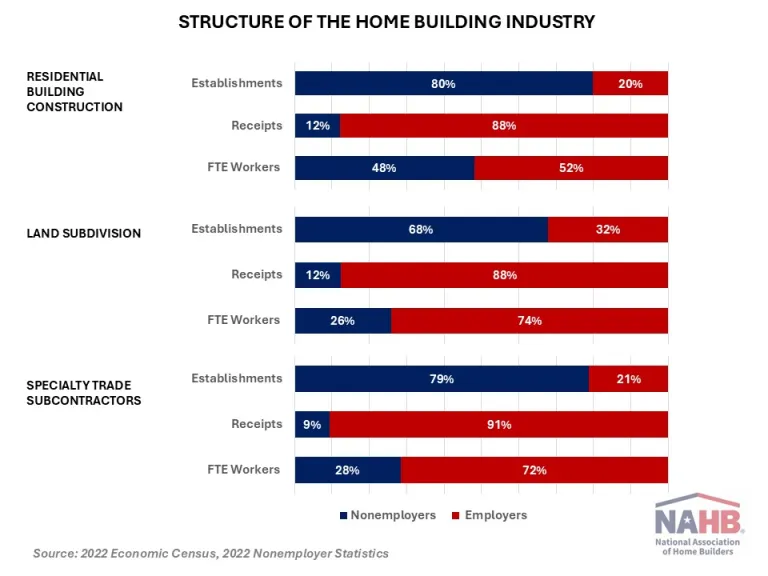

The latest estimates are based on data from the 2022 Economic Census and the Nonemployer Statistics Survey.

The Economic Census covers a number of construction subsectors within the home building industry:

- Residential Building Construction (RBC

- Single-family general contractors (excluding for-sale builders).

- Multifamily general contractors (excluding for-sale builders).

- For-sale new housing builders

- Residential remodelers and land subdividers (or developers)

- Specialty trade contractors (STCs)

According to 2022 figures, the vast majority of residential building enterprises are run by self-employed independent contractors.

There are about 813,000 nonemployer enterprises in residential building construction (RBC), which account for nearly 80% of all establishments.

More than 9,000 independent contractors make up 68% of land subdivision firms. Over 1.9 million specialty trade independent contractors account for 79% of all STC firms.

These non-employer enterprises also employ over half of all full-time workers (FTE) in residential building construction, 26% in land subdivision, and 28% in STC.

The majority of these self-employed mom-and-pop businesses are quite modest, with annual revenues averaging under $103,000 for residential building construction and $70,000 for specialist trade contractors.

Self-employed independent contractors in land subdivision generate an average of $288,000 in annual business revenue.

As a result, these nonemployer enterprises account for just 12% of total sales and receipts from residential building construction and land subdivision, as well as 9% of specialty trade contractors’ revenue.

Remodeling, land subdivision, and specialist trade subcontractors (STC) enterprises are often smaller than residential construction businesses with salaried staff.

Three out of four renovation establishments, 63% of land developers, and 59% of STC enterprises make less than $1 million in revenue.

Home builders are typically larger, with over 45% of enterprises reporting yearly sales above $1 million. Multifamily general contractors are often the largest segment of homebuilders.

However, the Census Bureau did not reveal the number of the greatest (with revenue greater than $100 million) and smallest (with revenue less than $100K) multifamily and single-family custom builders for 2022.

As a result, the revenue spectrum for MF and SF contractors is incomplete and shown in a separate chart.

Multifamily contractors are often larger than single-family contractors and for-sale builders (who build on their own property).

In 2022, 10% of multifamily contractors reported yearly revenues ranging from $10 million to $25 million, while another 11% earned between $25 million and $100 million.

According to the most recent Small Business Administration (SBA) size requirements, the great majority of residential construction enterprises are classified as small businesses.

The current small business size limits for all types of builders are $45 million, $34 million for land subdivision, and $19 million for specialist trade contractors.

According to these criteria, nearly all remodelers and single-family contractors, as well as at least 98% of land developers and 96% of specialist trade contractors, are easily classified as small firms.

The Economic Census, like many other federal statistics programs, only collects data from businesses who have payroll employees.

[Read more about this topic on Eyeonhousing.org]