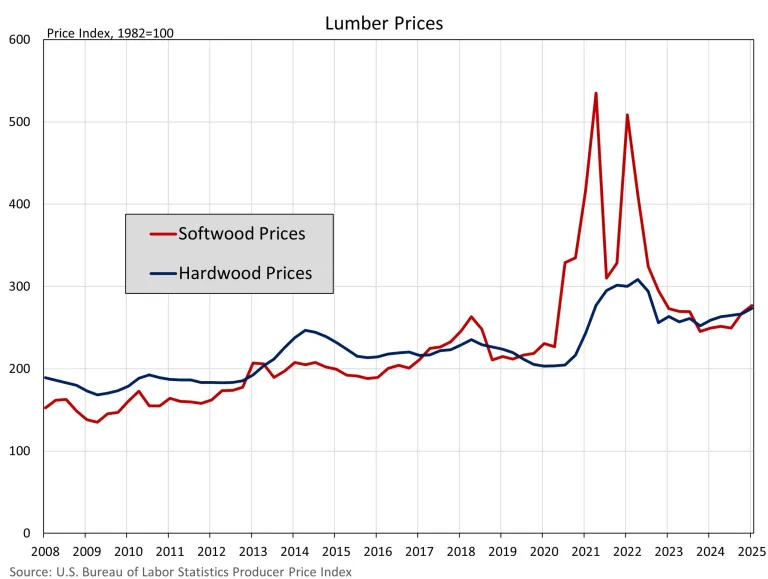

Lumber pricing uncertainty has risen since the beginning of the year, owing in part to projected higher tariffs, particularly on Canadian softwood lumber.

Despite the continual use and threat of tariffs, US sawmill and wood preservation industries have not boosted production to a level sufficient to replace imports.

In reality, utilization rates continue to plummet, indicating that they have the capacity to produce more lumber but are simply not working at that capacity.

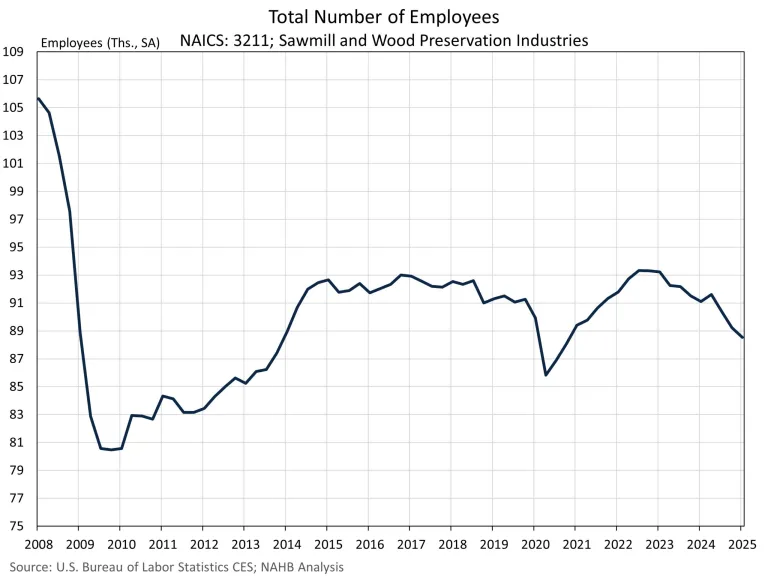

As these companies produce at lower levels, employment has decreased in recent quarters.

At the same time, limited international competition and artificially high prices have reduced enterprises’ incentive to expand output, even when demand remains robust. As a result, U.S. mills are still unable to meet the country’s total lumber consumption requirements.

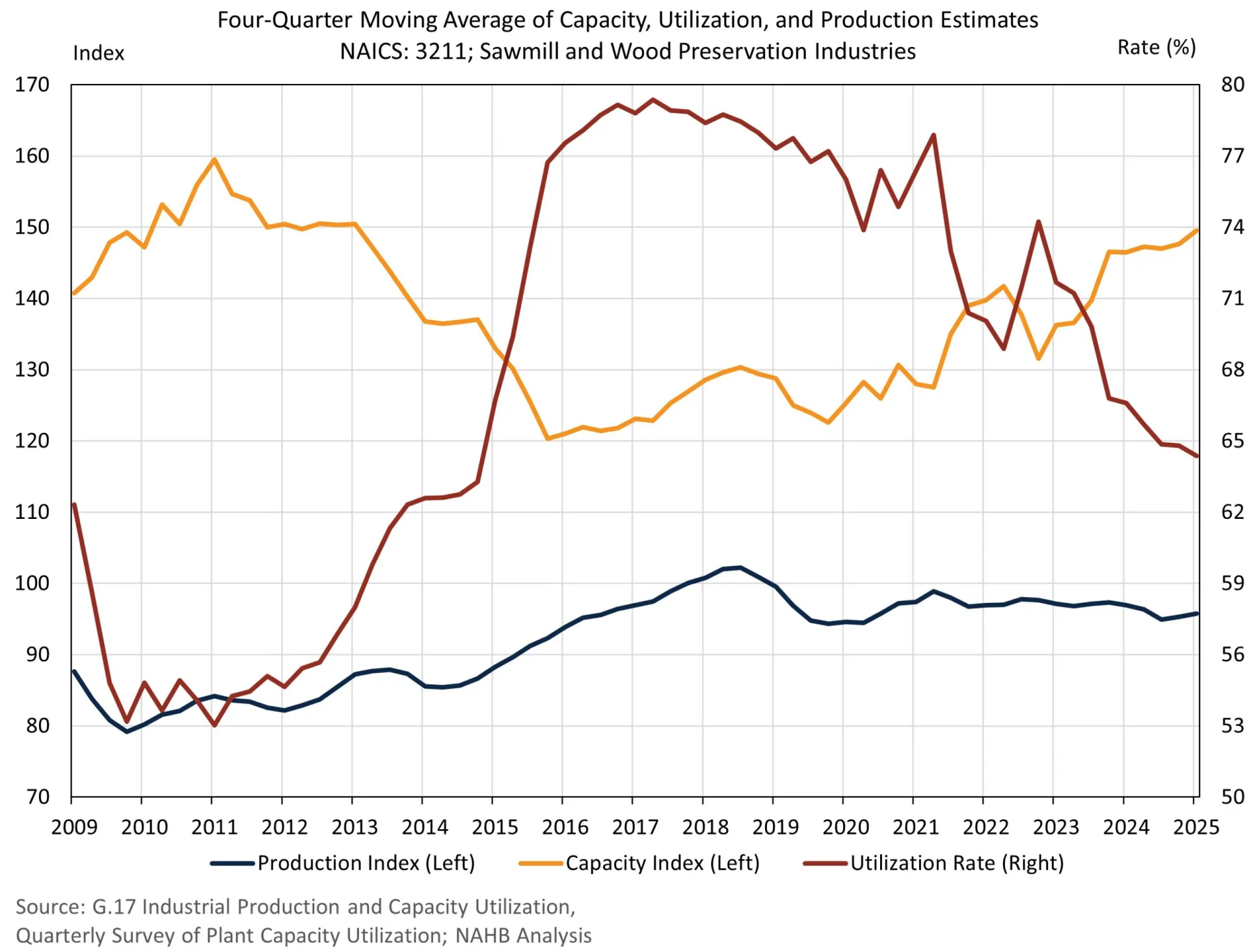

In the first quarter of 2025, sawmill and wood preservation companies reported reduced capacity utilization combined with sluggish production.

On a four-quarter moving average, the utilization rate, which is a ratio of actual production to potential production, was 64.4% in the first quarter.

The utilization rate has continued to fall since 2017, as capacity (or the ability to produce) has increased, but output has stayed lower than in 2018.

By combining the Federal Reserve’s output index with the Census Bureau’s utilization rate, we can construct a rough index estimate of the current production capacity of US sawmills and wood preservation enterprises.

A quarterly estimate of the estimated production capacity index is provided below, along with estimates of the production index and utilization rate.

Based on the data presented above, sawmill capacity has increased since 2015 but remains lower than peak levels in 2011.

The majority of recent capacity improvements occurred in 2023, with little gain during 2024.

As previously stated, there is plenty of space to enhance domestic lumber production, but existing production levels have remained relatively stable in recent years.

The Producer Price Index shows that lumber prices remain higher than in 2024.

At current pricing levels, producers may see little profit in boosting supply because it would drop prices, given that demand has fallen since the beginning of the year.

Notably, despite historically high prices in 2021 and 2022, producers were unable to raise production much during these periods, possibly due to supply chain problems.

In the first quarter, employment in sawmills and wood preservation firms fell to 88,533 workers. This is the third straight quarter in which employment in this industry has fallen.

Antidumping and countervailing tariffs have been in force since 2017 to defend the US lumber industry.

Tariff measures are normally supposed to give industry stability and increase jobs, but we are seeing the opposite.

These laws impose levies on imports of Canadian softwood lumber, which accounts for approximately a quarter of the U.S. softwood lumber supply. The current AD/CVD rates on Canadian softwood timber are likely to treble this fall, reaching more than 30%.

Because US timber production has been stable since the initial tariff policies were implemented in 2017, doubling these duty prices is unlikely to increase supply but would instead raise expenses.

[Read more about this topic on Eyeonhousing.org]