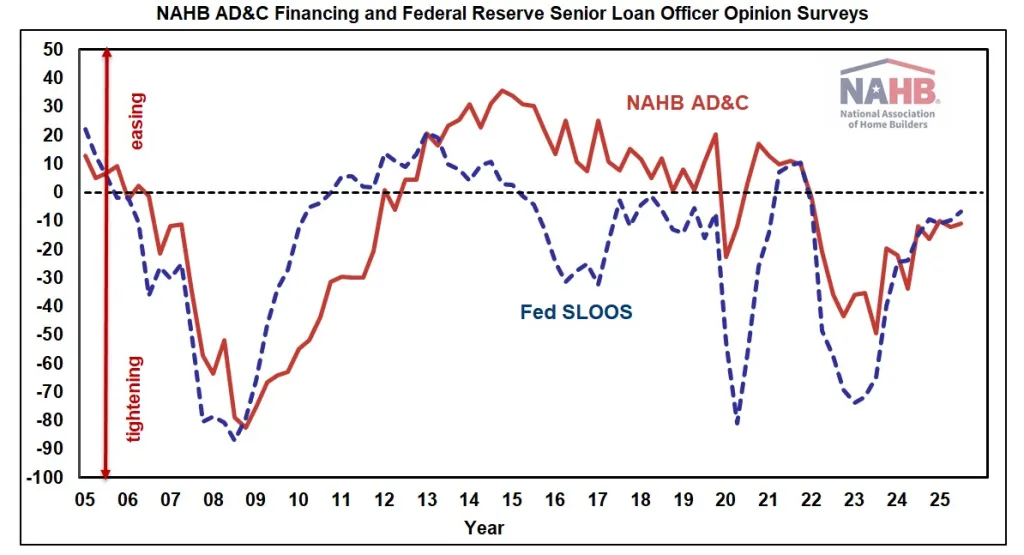

According to the NAHB’s quarterly survey on AD&C Financing, credit conditions for loans for residential Land Acquisition, Development, and Construction (AD&C) continued to tighten in the third quarter of 2025.

The survey’s net easing index came in at -11.0, showing that credit tightened since the previous quarter.

This is pretty close to the third quarter figure of -6.6 for the equivalent net easing index generated by the Federal Reserve’s poll of senior loan officers, indicating fifteen straight quarters of tighter credit conditions observed by both builders and lenders.

According to the NAHB poll, the most prevalent manner lenders restricted credit in the third quarter was to cut the maximum permissible loan-to-value or loan-to-cost ratio on loans (as indicated by 60% of builders and developers).

Reducing the amount they are willing to lend, requiring out-of-pocket interest payment or borrower funding of an interest reserve, and requesting personal guarantees were all noted by 47% of respondents.

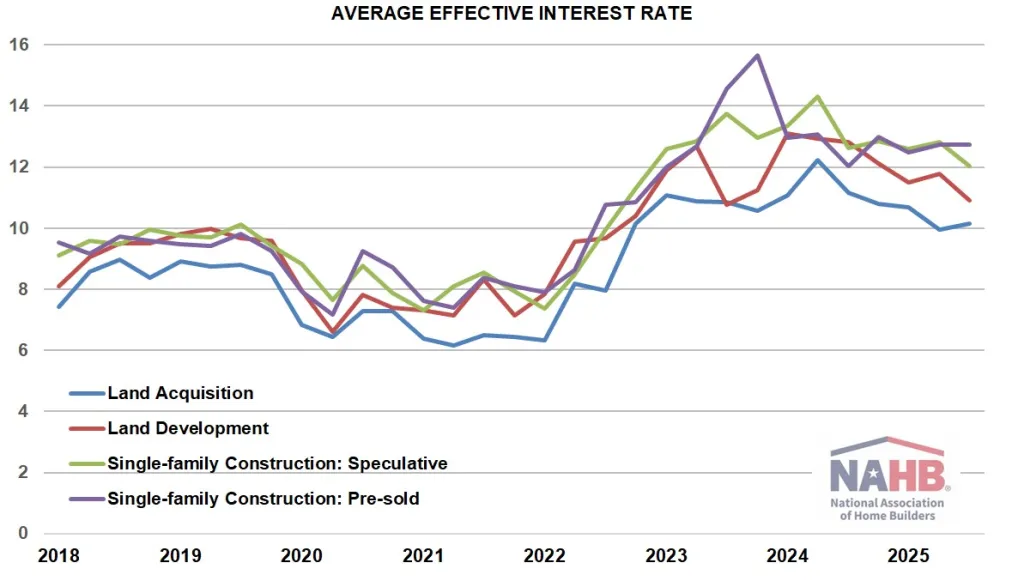

The third quarter’s credit cost results were mixed. The average contract rate rose from 7.82% to 7.95% on loans for residential land acquisition, but fell on the other three categories of loans tracked in NAHB’s AD&C survey: from 8.04% to 7.68% on loans for land development, from 8.17% to 7.90% on loans for speculative single-family construction, and from 7.95% to 7.90% on loans for pre-sold single-family construction.

Meanwhile, the average initial points charged on loans increased across the board: from 0.56% to 0.66% on land acquisition loans, from 0.74% to 0.83% on land development loans, from 0.72% to 0.74% on speculative single-family construction loans, and from 0.58% to 0.67% on pre-sold single-family construction loans.

These quarter-to-quarter changes caused the effective interest rate (which includes both the contract rate and the initial points) to rise from 9.95% to 10.15% on land acquisition loans, but to fall from 11.77% to 10.92% on land development loans and from 12.82% to 12.04% on speculative single-family construction loans.

The average effective rate for pre-sold single-family construction loans stayed almost steady at 12.74%, compared to 12.73% in the second quarter.

Although the average effective interest rate varied from quarter to quarter, the rate on each of the four types of AD&C loans has fallen significantly since peaking sometime between 2023 Q3 and 2024 Q2.

According to the NAHB AD&C survey, 37% of respondents who built single-family houses in the third quarter of 2025 reported financing some of the building with a construction-to-permanent (one-time-close) loan issued to the eventual home buyer.

On average, 63% of the residences built by these respondents were financed in this manner.

More information on credit conditions for residential builders and developers can be found on NAHB’s AD&C Financing Survey website.

[Read more about this topic on Eyeonhousing.org]