In January, new home sales experienced a decline, which was a result of weather-related disruptions and the typical monthly volatility.

Sales are broadly consistent with those of a year ago on a three-month moving average basis, indicating that underlying demand conditions have been relatively stable despite the month-to-month fluctuations.

In the interim, builders continue to depend on incentives to maintain demand and attract purchasers.

The January NAHB/Wells Fargo Housing Market Index revealed that 64% of builders utilized sales incentives, which represents the 12th consecutive month in which this percentage exceeded 60%.

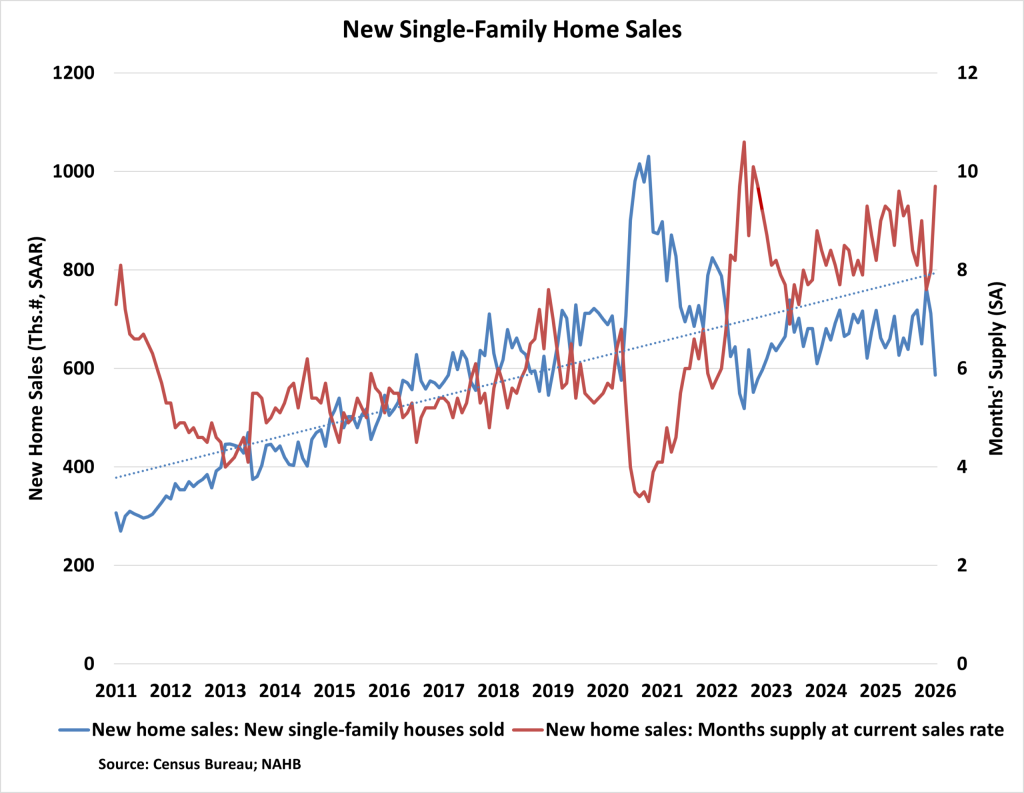

According to recently released data from the U.S. Department of Housing and Urban Development and the U.S. Census Bureau, the sales of newly constructed single-family homes decreased by 17.6% in January to a seasonally adjusted annual rate of 587,000, a decrease from a downwardly revised December reading.

The rate of new home sales has decreased by 11.3% from the previous year.

Sales were 688,000 on a three-month moving average basis, which is consistent with the 685,000 pace observed a year ago.

A new home transaction is initiated by the execution of a sales contract or the acceptance of a deposit.

The residence may be in any stage of construction, including not yet initiated, under construction, or completed.

The January reading of 587,000 units is the number of residences that would sell if this pace were to persist for the next 12 months, in addition to accounting for seasonal effects.

In January, the inventory of new single-family homes increased to 476,000 units. This is 0.4% higher than the previous month, but it is 4.0% lower than a year ago.

The months’ supply of new residences was 9.7 at the current sales pace, which is an increase from 9.0 a year ago.

The transient slowdown in the new home market, which was partially reflected in the increase in inventory and weaker sales, was exacerbated by weather disruptions that restricted transactions throughout the month.

Sales in regions such as the Northeast experienced a significant decline of 44.7%.

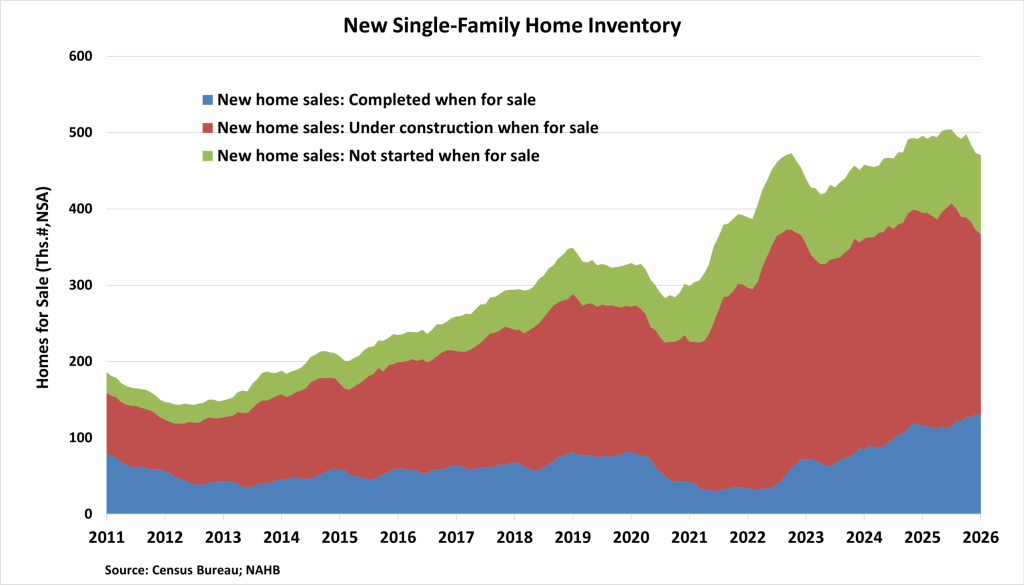

There were 116,000 completed, ready-to-occupy residences available for sale last year (not seasonally adjusted).

The figure had risen by 10.3% to 128,000 by the conclusion of January 2026. Nevertheless, residences under construction comprised 51% of the total inventory, while completed, ready-to-occupy inventory constituted only 27%.

The remaining 22% of new homes for sale in January were residences that had not yet begun construction at the time of the sales contract.

The median new home sale price decreased by 4.5% to $400,500, which is a 6.8% decrease from the previous year.

In January, 19% of new residences were priced below $300,000, while 34% were priced above $500,000. Since October 2025, the proportion of new residences priced below $300,000 has declined, following a recent high of 23% in September 2025.

Year-to-date, new home sales have increased by 1.4% in the Midwest and 4.1% in the South on a regional scale.

The Northeast has experienced an 8.3% decline in new home sales, while the West has experienced a 3.5% decline.

[Read more about this topic on Eyeonhousing.org]